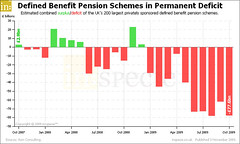

After the town hall meeting I attended on Wednesday I have been thinking about pension plans generally. The state of Utah is looking at changing their pension offerings for new employees to save the state from future financial ruin. I have seen other companies go through that process already. As a nation we have seen the cost of defined benefit pensions contribute mightily to the downfall of GM and Chrysler as well as having a hand in the struggles throughout the airline industry not so many years ago.

As I thought about all these examples I realized that even a fully funded defined benefit pension program is a gamble for any organization. Employees like the security, but it is an inherently risky proposition to offer such a plan.

I decided to look into the history of pensions and as with so many other systemic problems we face, the problem of widespread pension offerings really took root as a result of a poorly conceived government intervention, namely wage freezes during WWII where companies began exploring new ways to compensate workers besides simply using salary as compensation. Notice that this is also at the root of our dysfunctional employer-dependent health insurance boondoggle. The fact that both of these crippling trends were incubated by government wage interference and nursed along afterward through favored status in our tax policy should be a major red flag against further socialist economic moves by our government – no matter how good it might look now there is bound to be a crippling downside that will rear its ugly head later.

That’s a great point. Government intervention during World War II has had massive, rippling, unintended economic consequences.

The worst part of it is that the government reaction to those unintended consequences is always to double down.

I don’t agree here. You can’t single out one item like pensions, and say that that particular cost is what caused the downfall of GM or any other industry. Providing your employees security in their old age is a choice. It is one of the things a company can choose to spend its money on, just like executive compensation, private jets, bonuses, or purchasing other companies. The investment risk posed by defined benefit pension plans is actually less than that posed by the typical 401K plan because the defined benefit plan typically has a well-informed professional management overseeing its investments. 401K plans shift the investment risk to the worker who is not generally well equipped to manage it.

Having given companies and employees incentives to move from defined benefit to defined contribution plans, only the still-unionized government sector employees have real retirement security. Sacrificing their retirement security in the name of personal independence is wrong and violates the contract made with these workers. Instead of that, we should be looking to the government to insure everyone’s retirement and health security and distribute the cost equitably across the population. Socialism here is the answer, not the problem.

First of all, I did not single out pensions as the particular cost that caused the downfall of GM – I said it was a major contributing factor, as evidenced by that fact that getting the pensions off their books was one of the major concessions they won to get out of bankruptcy.

Shifting from defined benefit to defined contribution does place the risk on the employee – the point is that defined benefit poses too much risk for companies. Eventually they will suffer for taking that risk. Who’s responsibility is my retirement security? Is it the responsibility of my company, or is it my responsibility (whether or not I am competent to manage a 401K)?

Many (meaning large numbers, I’m making no claim about percentages) workers who retired with defined benefit pensions later found their companies going bankrupt or offloading the pension obligations to another entity, usually the government. Every time that happens is evidence that no mater what the contract says, there are no future guarantees – that’s why defined benefit pensions are not a wise company policy – no matter how much the workers may like them.

Socialism is not the answer here. No matter how far you spread the cost it will eventually grow to the point of bankrupting whoever is responsible for it – unless the responsibility falls to the individual. If the responsibility lies with the individual rather than the government or the employer some people will still go bankrupt, but not everyone. If we apply socialism eventually everyone will go bankrupt and have a lower standard of living.

Obviously we disagree, but that’s what makes discussion fun. If I as an employer sign a contract that makes me responsible for the retirement security of my employees, then I should not be permitted to avoid that responsibility. In a number of cases, companies went bankrupt primarily to invalidate labor and pension agreements so they could increase profits. They went bankrupt for the same reasons anyone does, they spent money they didn’t have, made risky investments that didn’t pay off, and it caught up with them. IMHO, their obligation to their employees far outweighs that to their stockholders.

Socialism in this case is just like insurance (or how insurance is supposed to work). By spreading out the risk, it is possible to offer life insurance even though we know ever person is going to die eventually. If we tax appropriately and provide everyone with retirement and health security then we can be sure that no one will have an unacceptably low standard of living. That may preclude the privileged few from having an extremely high standard of living but that is a small price to pay. Perhaps a government that puts the security and health of its people first will have a high marginal tax rate and will not be able to afford to spend a trillion a year on its military, but it won’t go bankrupt.

I agree that if an employer signs a contract they are responsible for whatever they promised. My contention is that long-term and widespread, no company can keep such a promise – no matter how good their intentions. Having signed such a contract I agree that they bear higher responsibility to their employees than to their shareholders, but I still say that is a promise they cannot guarantee to keep.

I recognize that there are those instances where companies enter bankruptcy jost to offload those kinds of contractual obligations but my argument here is that even if they did not do that they would eventually find themselves unable to pay – even if they agree with us that their first obligation is to the employees they have promised to pay.

I disagree. A government that puts the security and health of its people first by having a high marginal tax rate and not spending a trillion a year on its military will still run a risk of going bankrupt – no person, nor any collection of people can make such a promise indefinitely because they cannot control the future. Making promises that depend on things that have not yet happened is inherently risky. You compare it to insurance – fair comparison. Is there some rule out there that guarantees that no insurance company will ever go bankrupt if they simply follow some known set of rules? The answer is no. I’m saying that the government cannot make a promise any more than a company. Things can happen outside their control that may prevent them from keeping their promise because there is no such thing in real life as a truly closed system.

401K’s are just as big a failure as pension funds, only difference is people who’s 401K’s dump out loose their retirement rather then like in a pension fund where the employer eats the loses. The only long term sound retirement system in the United States in Social security. SS does need some fix’s, mostly they need to make the FICA tax’s applie to all income sources and not just payroll income.

I agree with Charles, I would like to see a insured retirement fund that is not tied to an employer. Its unreasonable to think people should understand enough to accurately manage their market invested retirement. I would like to see both insured and non insured retirement investments, if someone thinks their good enough with the market to risk a higher paying uninsured account let them. Retirement planning should be simple, its crazy to think everyone has to take the a 20-40 year projection of what the market will be like when they plan their retirement.

Nothing wrong with Social insurance, in the case of retirement its good sound thinking to go that way. Also If peoples retirements are in Social insurance if the market craps out due to bad banks its easier to let the banks fail as the nations retirement system won’t depend on them. IMO that sounds like a good way to prevent national fiscal emergency’s. One of the biggest reasons TARP was needed was because of retirement investment’s held by those banking institutions could not be allowed to be destroyed. I could just imagine what would have happened if 50 Million peoples retirement’s disappeared overnight because we didn’t bail the banks out.

“I disagree. A government that puts the security and health of its people first by having a high marginal tax rate and not spending a trillion a year on its military will still run a risk of going bankrupt – no person, nor any collection of people can make such a promise indefinitely because they cannot control the future. Making promises that depend on things that have not yet happened is inherently risky. You compare it to insurance – fair comparison. Is there some rule out there that guarantees that no insurance company will ever go bankrupt if they simply follow some known set of rules? The answer is no. I’m saying that the government cannot make a promise any more than a company. Things can happen outside their control that may prevent them from keeping their promise because there is no such thing in real life as a truly closed system.”

Governments exist for hundreds of years, business’s rarely exist on this scale. Governments have tools to control risk beyond what business’s can do. They have the ability to control the currency, set laws/regulations, control tax rates etc Governments are very suited to this sort of thing.

While I might argue that in spite of the fact that we cannot predict the future and that insurers go bankrupt from time to time, we still buy insurance and pay premiums in the hope (?) that when we die, our families will be paid the amount agreed upon. But I will argue that a government, particularly the US government, operates according to a different set of rules than an insurance company. The government can print money (indirectly at least) and always has the capability to reorder priorities, raise taxes, or borrow the money necessary to meet its obligations. In addition, the US dollar is still the world’s reserve currency and other nations need dollars and need dollars to actually have value. The US is not in danger of bankruptcy, and very few if any major governments in the industrialized world have ever faced such a prospect.

The Social Security system is an excellent example here. Very conservative investments were made and with an adjustment a few decades ago in the supporting tax, a large reserve was developed. Now even though the baby boomer generation is retiring, the system still can pay all the benefits to all the retirees for at least another 25-30 years. At that point, there will be a brief period where the system will not be able to pay the full benefit but as we old folks die off, they’ll go back into the black. If there were political will, even that brief period could be brought up to full benefit level by simply eliminating the salary cap on the payroll tax so that every wage earner paid the same rate. It’s not a perfect system, and the benefits though rather generous, cannot provide a comfortable retirement in every case. The model is proof that governments can keep promises even though they cannot foresee the future.

Both of you rightly acknowledge that businesses are different than governments but you don’t seem to admit that differences included governments are not immune to external forces. You cite control of currency as a factor that favors governments but you fail to recognize that currency has no inherent value. For example, the government can print all the currency they want and it will do no good in the face of a sustained drought.

The argument that the government can always “reorder priorities, raise taxes, or borrow the money necessary to meet its obligations” is plainly false. (“Always” is a dangerous word when making an argument.) The truth is the the U.S. government can currently reorder priorities, raise taxes, or borrow money, but there is no guarantees in the future that that will remain the case. Currently the U.S. dollar is the world’s reserve currency which has been very beneficial to us, but there is nothing to guarantee that the rest of the world will never dump the dollar as their reserve – in fact they are almost sure to do so if they ever begin to believe that our government is pursuing an economically unsustainable path.

My understanding of social security is that virtually the entire reserve has actually been loaned out to the rest of the federal government and currently consists only of promises for repayment. That’s why we have had years of politicians talking about creating a “social security lock-box.” If nothing happens to cause the rest of the system to falter there will be enough for another 25 – 35 years, but actual cash reserves are much lower. If you can prove me wrong I will stand corrected on that.

The fact is that if social security were structured as insurance, where everyone paid in but only those who failed to save for retirement were given benefits (preferably enough benefit to survive but less than most people might reasonably be able to save on their own over a working lifetime), it would be a lot more sustainable. Life insurance does not pay out to most people who get it – they get term life policies and then fail to die during the term of coverage. Not very many people pay the vastly higher premiums of a whole life policy. That is the same failing of our current notion of health insurance – it’s not insurance because it is expected to cover everyone all the time rather than covering only those people who face some atypical medical need. Many people go their entire lives without making a claim against their home or car insurance, but the only people who make no claims against health insurance are a portion of those who never have health insurance.

David, all Treasury bills regardless of whether they are held by you and I, the Chinese banks or the Social Security trust fund are simply promises of repayment with interests, like any other bond. The National Committee to Preserve Social Security and Medicare says “For nearly three decades, Social Security has taken in more revenue each year than it has paid out in benefits. These excess funds have been invested in special issue U.S. government securities. Thus, Social Security has effectively been loaning its excess funds to the federal government to spend on other programs. Rather than increasing the federal deficit, Social Security’s annual surpluses have actually been covering up the true size of the deficit in the general fund.” There has definitely been some “creative accounting” at work, but that doesn’t relieve the government of its obligations.

As for your other objections, if social security had been needs tested it would never have passed. It works because every American has the opportunity to benefit, but many never do. People die without survivors, social security taxes are paid by non-citizens who are not entitled to benefits, many people die before they recoup anything like the money they paid in. All these factors make it possible for the system to pay benefits for decades to citizens who qualify and to provide support to those unable to fend for themselves or for the families whose breadwinner has died early.

Nothing can be predicted with certainty about the future, but if we hunker down and take the most pessimistic outlook on our economic and financial future, we will be at a great disadvantage. There is no investment without risk, and if we fail to accept reasonable risk we will make no investment and reap no reward. The question is not whether the government should spend money, but whether the money it spends is an investment in our future, or waste and corruption. Making sure Americans have access to quality health care and have financial security in their old age are good investments that help everyone. I’m sure we both could make a long list of government expenditures that will never provide benefit to ordinary Americans.

I know that all T-bills are promises of repayment – that does not change the fact that the Social Security surplus is nothing but promises. How many businesses fail not because of lack of revenue, but because income they have rightfully earned was not repaid in a timely manner. You may trust that the federal government can maintain their creative accounting indefinitely but I don’t. One day the piper will have to be paid.

The fact that the system is dependent on people failing to collect promised benefits and paying when they should not even be here shows the weakness of the financial position of this “model” program. Once again I am left wondering if anyone could design a system with a shakier foundation.

I agree there are risks that need to be taken and that we must invest in our future, the difference between us is what is considered an investment and what is considered foolish idealism by our politicians.

I’d like to see your list of government expenditures that never provide a benefit to ordinary Americans – especially if you have some that I don’t already have on my list of programs that should be cut.